There’s no shortage of noise in fintech branding. Big claims. Disruption narratives. Technology framed as the answer to everything.

In financial services, that approach erodes confidence.

Between 2020 and 2026, the fintech market split. Capital began flowing toward businesses with clear fundamentals, disciplined governance and credible paths to profitability. The growth-at-all-costs narrative lost momentum. Investors prioritised resilience, repeatability and operational strength. In practical terms, they prioritised institutional trust.

The psychology of institutional trust.

When Kraken raised $500 million at a $15 billion valuation in September 2025, the inflection point wasn’t a feature release, but rather regulatory credibility. Wyoming charter. MiCA approval. Proof-of-reserves audits. The company leaned into being one of the most regulated exchanges in its category while others emphasised disruption.

Institutional psychology follows a pattern. Academic research from the Review of Finance suggests that investors allocate more capital to managers they trust, even when those managers charge higher fees. So, trust increases perceived reliability. It supports larger capital commitments, shifting focus from price sensitivity to long-term stability.

When you’re marketing financial services, speed and novelty carry less weight than proof of protection. Consumers and institutions evaluate risk first. Confidence follows evidence. Trust has always sat alongside price and quality as a primary purchase driver. And service quality alone doesn’t create that trust. Positioning does.

Trust in financial services is built deliberately. It runs through your messaging, your compliance posture, your governance structures and your operational decisions. Without that alignment, innovation-led narratives increase perceived risk rather than reduce it.

When sameness dilutes value.

From 2020 to 2023, a wave of fintech unicorns experienced substantial valuation corrections. Valuations reset. Market dynamics played their part. Positioning did too. Many businesses had driven rapid adoption, fuelled by sharp incentives and strong momentum. But fewer had boosted their brand equity with the clarity and distinction that holds firm when conditions shift.

Adoption might move fast, but brand equity compounds. So, when multiple neobanks framed themselves as the modern alternative to traditional banks, the category blurred. Messaging started to echo. Differentiation thinned out. Growth leaned heavily on promotional mechanics because the brand story lacked separation. As incentive budgets narrowed, that growth proved harder to sustain.

In B2B fintech, the stakes rise further. Corporate treasurers, procurement leads and risk committees answer to boards and regulators. Every decision carries professional weight. Selecting a partner that signals stability, credibility and shared consensus protects reputations as well as balance sheets.

Research continues to show that B2B decision-makers prioritise brand trust and familiarity when building a shortlist. If your positioning blends into the wider category narrative, you make it harder for buyers to advocate for you internally. Distinction gives them confidence.

The compliance shift.

In the 2020s, compliance moved into clear view. What once sat in the background became part of how you signal strength to the market.

In the early stages, it was easy to frame compliance as cost control. But as the market matured, that mindset evolved. The companies that invested visibly in compliance infrastructure were commanding stronger valuations. Regulatory depth started to signal operational maturity. It showed you were building for scale, with the governance to match your ambition.

Polymarket reflects that trajectory. After regulatory enforcement restricted U.S. access, the business rebuilt its footing from the ground up. It invested in licensed infrastructure, acquiring QCEX for $112m – a CFTC-regulated exchange and clearinghouse – creating a compliant framework for U.S. operations.

That move reset how the market valued the company. With a formal compliance system in place, Polymarket secured up to $2bn in investment from Intercontinental Exchange, valuing the business at around $8bn and positioning it within mainstream financial infrastructure.

Backing at that level signalled institutional legitimacy. It widened Polymarket’s reach beyond retail users and reinforced its readiness to operate in regulated markets.

Regulatory depth, handled this way, becomes infrastructure. It signals operational maturity. And it opens the door to institutional capital. And the valuations that follow.

Even more, across the ecosystem, higher-valued fintechs reshaped their narrative in similar ways. Stripe positioned itself as core financial infrastructure, embedded in the global economy. Revolut amplified its regulatory depth and operational scale. The market responded to businesses that aligned bold ambition with institutional-grade discipline.

Compliance became a visible marker of credibility. Documented. Verifiable. Part of the story you tell investors, partners and customers alike.

From compliance to category leadership. Sharpening strategic positioning.

Regulatory depth builds credibility. But credibility alone doesn’t secure premium positioning. To command institutional trust at scale, you need strategic clarity. You need to define the space you occupy.

This is where leading fintech brands separate themselves. They move beyond competing on features and parity within crowded peer groups, and instead sharpen their positioning around what they uniquely enable. That position is shaped by their strengths, governance model and long-term priorities.

When you shift the conversation away from feature comparison, you change how you’re evaluated. You reduce direct substitution. You anchor your offer in a narrative aligned with institutional logic rather than product checklists. You’re no longer weighed against peers on incremental differences. You’re understood on your own terms, for the role you play and the value you create.

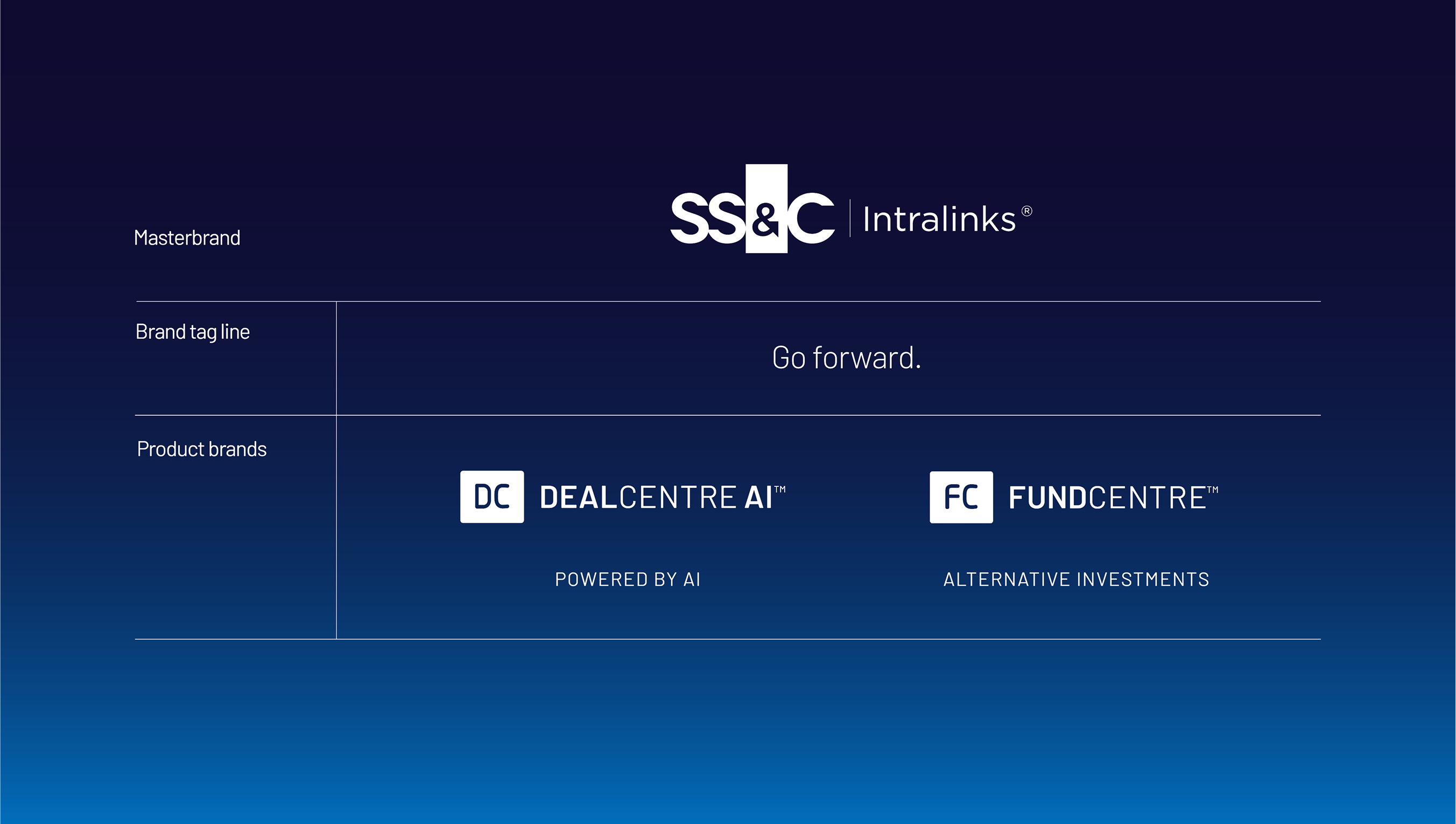

For example, when we partnered with SS&C Intralinks to redefine their masterbrand, it built on a relationship already proven in market.

We had previously rebranded Intralinks, a move that sharpened their position and helped drive valuation from £1bn to £1.5bn within 11 months, ahead of their acquisition by SS&C. The brand and the business moved in sync. The market responded.

When they came back to us, the challenge had shifted.

The business had evolved into a fully integrated dealmaking ecosystem. DealCentre. FundCentre. Proprietary AI. Powerful. Connected. But the masterbrand wasn’t yet telling that story as one.

So we built a cohesive architecture. One ecosystem. One narrative. One elevated promise. Every product and capability aligned under a sharper proposition, reflecting the scale, intelligence and authority of the platform as a whole. No fragmentation. No internal competition. Just a clear commercial story that reframed SS&C Intralinks from a suite of tools into the reference point for intelligent, secure dealmaking.

That clarity positioned the business not as one of many VDR providers, but as the infrastructure powering modern transactions at scale.

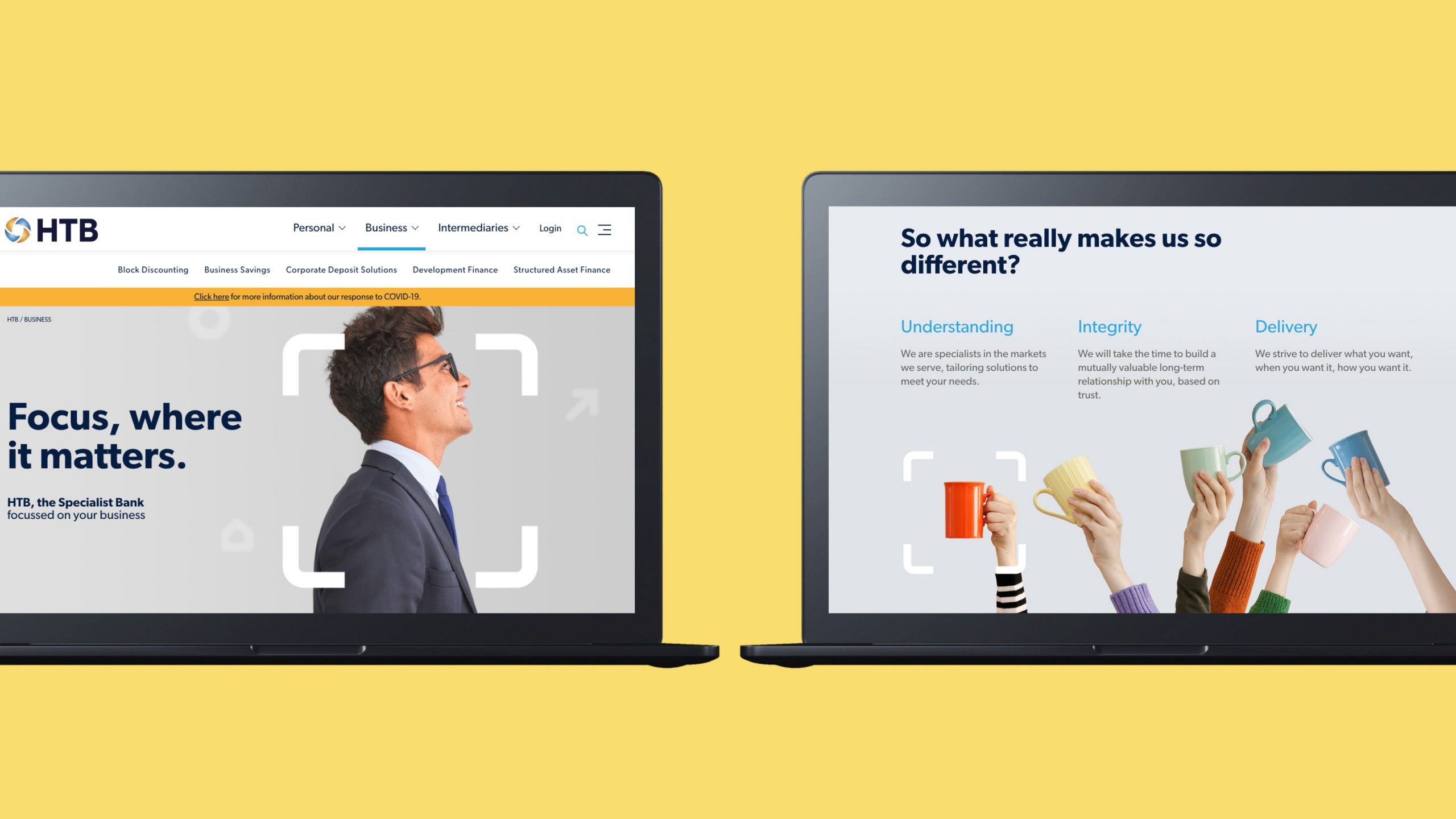

We saw the same principle at work with Hampshire Trust Bank. Rather than competing on breadth, we defined their proposition as “excellence through specialism”. The visual and verbal system reinforced depth, expertise and disciplined focus. The bank stepped out of the generic challenger narrative and into a position centred around authority.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Institutional financial services and fintech brands that command premium positioning shape the frame through which they’re judged. They define the criteria and control the context.

Building institutional trust into your brand.

If you’re shifting from broad innovation messaging toward institutional credibility, you need structure behind the story. Because trust at scale doesn’t just happen. It’s designed – engineered across every touchpoint.

It begins with how you position yourself. When you look at your brand through an institutional lens, stability, governance and long-term resilience move to the forefront. Generic category language falls away. What remains is clear proof that your model holds up under scrutiny, not just in a pitch deck but in practice.

From there, trust needs to be visible. Licences, certifications, independent audits, institutional partnerships and referenceable clients carry weight when they’re surfaced with clarity. Institutional buyers look for signals they can validate and stand behind internally. When those signals are easy to find and easy to evidence, confidence builds.

Your positioning then sharpens the frame. A defensible specialism, aligned to your strengths and governance model, gives your brand focus. When that focus runs consistently across product, marketing and leadership communications, it creates coherence. And coherence builds credibility.

Over time, relationships become part of your story. Institutional buyers commit to partners who demonstrate operational maturity, financial stability and sustained client partnerships. Recognition grounded in substance reinforces that narrative. It shows you’re made for endurance, not short-term noise.

Trust scales when perception and performance align. And when your positioning reflects how you operate day to day, credibility compounds.

Let’s get things Done & Dusted.

In the financial sector, generic branding blurs distinction, weakening internal advocacy and leaving valuation exposed to market shifts. When capital flows toward resilience and governance, your brand needs to signal both with clarity.

That’s where we come in.

We work with fintech and financial services businesses at pivotal moments of scale. When compliance becomes strategy. When innovation needs institutional framing. When ambition calls for sharper definition. We align positioning with operational reality, simplifying complex architectures and defining Distinctly Different propositions that hold up under scrutiny.

If you’re ready to strengthen institutional trust, sharpen your positioning and build a brand that carries weight with investors, regulators and buyers alike, let’s talk.

Contact us today and let’s assess what your brand needs to take its next step.

Ready when you are.