Branding accounts for more than 30% of market value in leading companies, with over three-fifths of CEOs attributing more than 40% of valuation to brand and reputation.

In a market where strategic acquisitions made up 78% of fintech exits in 2025, these facts go beyond marketing theory. That’s simply the reality of the deal.

And in this reality, scale-ups that command premium multiples start early. 12-24 months out, to be precise. Those who wait until even six months before due diligence often find buyers reframing the narrative for them. And discounting accordingly.

That 12-24 month window is all about building a coherent, credible business story where brand, operations, governance and financial performance reinforce each other. Because a strong exit is rarely improvised in the final stretch. It’s built carefully and with purpose.

This is your brand readiness playbook for exit, where, rather than working in isolation, your brand is the organising system that aligns perception, performance and proof.

The ultimate exit brand readiness playbook.

Months 24-20: Define your strategic narrative.

At the two-year mark, clarity is your number one priority.

This is the stage where you step back and assess the business as an investor would. Not just how it performs, but how it’s perceived, structured and understood.

Begin with a comprehensive brand and business audit examining external perception, market positioning, competitive differentiation, internal alignment and operational maturity.

- Where is the story clear?

- Where does it fragment?

- Where do teams interpret it differently?

This baseline will shape every future discussion with buyers or public market investors. It highlights the gaps that need tightening before scrutiny begins.

In parallel, leadership must align on a defined exit thesis. A focused articulation of your strategic value. And to whom it benefits.

For acquisition-led strategies, this means identifying the financial institutions, payments networks or fintech platforms whose growth agendas align with your capabilities. The narrative should show how your tech, regulatory credibility, customer base or data assets strengthen their roadmap and reduce their execution risk.

For IPO preparation, the lens shifts. Institutional investors look for defensibility, scalability and predictability. Durable revenue. Clear governance. Credible expansion plans. The story you tell must be supported by evidence.

With direction agreed, you need to formalise governance structures. Clarify decision-making authority across brand, product and corporate communications. Align internal teams around a single, consistent narrative so that customers, partners and investors encounter one coherent version of the business.

This phase ends with a structured brand valuation exercise that:

- Quantifies brand equity’s contribution to enterprise value.

- Assesses its influence on customer acquisition efficiency, pricing power and retention strength.

Independent validation at this stage builds credibility and reduces friction later, when scrutiny intensifies.

By the end of months 24-20, the ambition is clear. The narrative is aligned. And the groundwork for exit readiness is in place.

Months 20-16: make trust measurable.

By this point, you’ve defined the story. Now you need to prove it.

Between months 20 and 16, the focus shifts from articulation to evidence. Trust can no longer sit in the realm of reputation or anecdote. It needs to show up in your data, your processes and your reporting.

Start with visibility. Strengthen your CRM and data infrastructure so that you have a clear view of customer journeys, retention patterns and lifetime value. Move beyond headline growth figures by:

- Tracking churn by segment.

- Analysing expansion revenue.

- Identifying the behavioural signals that predict renewal or risk.

Because when you can demonstrate disciplined oversight of revenue predictability, you reduce uncertainty in the eyes of investors and acquirers.

Next, formalise customer engagement. Structured loyalty or advisory programmes should generate strong, verifiable retention data, backed by documented reasons for why customers stay and why they leave. This will lower perceived integration risk, while also signalling embedded relationships that competitors will struggle to displace. That resilience has a direct impact on valuation confidence.

Regulatory maturity also becomes more visible during this phase. You’ll need to go beyond minimum compliance requirements by:

- Strengthening SOX readiness where relevant.

- Enhancing KYC and AML processes.

- Maintaining robust privacy standards across GDPR, CCPA and emerging jurisdictions.

Just as importantly, make sure to document these frameworks clearly. Potential acquirers should be able to review your compliance architecture and understand it without ambiguity. Clarity reduces friction.

Your governance and reporting cadence should now reflect institutional standards. If you are IPO-bound, begin operating with quarterly discipline before you are required to do so. Establish KPI dashboards covering transaction volume, customer acquisition cost, lifetime value and churn as core management tools. Even if acquisition is the likely route, this level of transparency signals operational control and readiness for integration into a larger organisation.

By the end of months 20-16, trust should not rely on reputation alone. It should be measurable in your systems, visible in your reporting and defensible under scrutiny.

Months 16-12: align performance with promise

At this stage, buyers and investors are stress-testing your ability to deliver it at scale. They will look closely at whether your growth is repeatable. Whether quality holds under pressure. And whether profitability improves as you expand.

This is where positioning and performance must line up.

Start with operational discipline:

- Tighten financial close cycles.

- Streamline onboarding processes.

- Reduce error rates across customer touchpoints.

If you are preparing for IPO, aim to outperform industry norms on reporting timelines. Shorter, cleaner close cycles signal financial control and organisational maturity. They show that the business is built to operate under scrutiny.

Next, focus on unit economics. Document customer acquisition cost, lifetime value and your LTV-to-CAC ratio, ideally at or above 3:1. In the current market, growth alone does not carry valuation weight. Investors are looking for sustainable margins and a clear, credible path to profitability. Your numbers should demonstrate that the model scales efficiently, not expensively.

You’ll also need to address customer concentration risk during this window. If a small number of clients account for a disproportionate share of revenue, diversify:

- Expand geographically.

- Deepen into new verticals.

- Introduce complementary product lines.

Visible diversification reduces valuation sensitivity during due diligence and strengthens negotiating position.

We saw this play out with AutoRek, a fintech pioneer whose technology transformed slow, compliance-risky manual tasks into seamless automation, earning trust across Europe's top-tier banks. But cracking North America meant navigating uncharted territory. No reputation. Minimal awareness. And a vast cultural divide.

We repositioned the business around the organising idea “Be sure”, driving a full rebrand, website overhaul and launch campaign in North America. Within 12 months, revenue increased by 21% and six major North American clients were secured. The repositioning sharpened perception. The operational expansion improved revenue quality, strengthening their overseas expansion.

At this stage, the objective is simple. Ensure that what you say about the business is supported by how it performs. Under scrutiny, alignment is what holds value in place.

Months 12-8: strengthen market authority.

With around a year to go, the foundations should be in place. Structure defined. Governance tightened. Performance improving.

Now the focus shifts outward.

This is the stage where you ensure the market sees the business the way you want investors and acquirers to see it.

Start with clarity. Communicate your strategic positioning consistently across every touchpoint. If you’ve consolidated under a masterbrand, explain why. If you operate a portfolio of products, articulate the logic behind it. Customers, partners and analysts should understand how the pieces fit together and where the value sits. Ambiguity at this stage creates doubt later.

Next, build visible authority. Position your senior leadership in the right rooms and conversations. Industry conferences. Analyst briefings. Targeted commentary in trade media. Not generic exposure, but informed perspectives that demonstrate you understand your market, its risks and its direction of travel. Third-party validation strengthens credibility and supports both acquisition discussions and IPO momentum.

If your earlier audit identified the need for a rebrand or a brand refresh, this is the window to implement it. Twelve to eight months provides enough time for perception to shift and for the updated positioning to be reflected in customer and partner conversations. Leave it too late and it risks appearing reactive rather than strategic.

Finally, formalise customer advocacy. Develop detailed case studies with named clients and quantified results. Show the outcomes you’ve delivered. Reduced processing time. Lower operational costs. Improved compliance. These materials provide external proof points and reduce perceived implementation risk during diligence.

By the end of this phase, your internal alignment should be matched by external credibility. The market should recognise the maturity you’ve been building behind the scenes.

Months 8-4: prepare for scrutiny

From month eight onwards, the emphasis shifts from optimisation to proof.

At this stage, readiness is about documentation. Everything you have built over the previous 16 months needs to be organised, evidenced and easy to interrogate.

Start by establishing and populating your virtual data room with structured materials covering strategy, governance, financial performance, customer acquisition, competitive positioning and intellectual property. The way you organise information signals how well the business is run. Clear structure reduces friction.

Pay particular attention to intellectual property. Ensure trademarks are registered, domain names are secured and IP assignments are formally completed and held by the company. Gaps in documentation often lead to valuation adjustments to account for remediation risk. Clean, comprehensive IP records protect deal certainty and preserve negotiating strength.

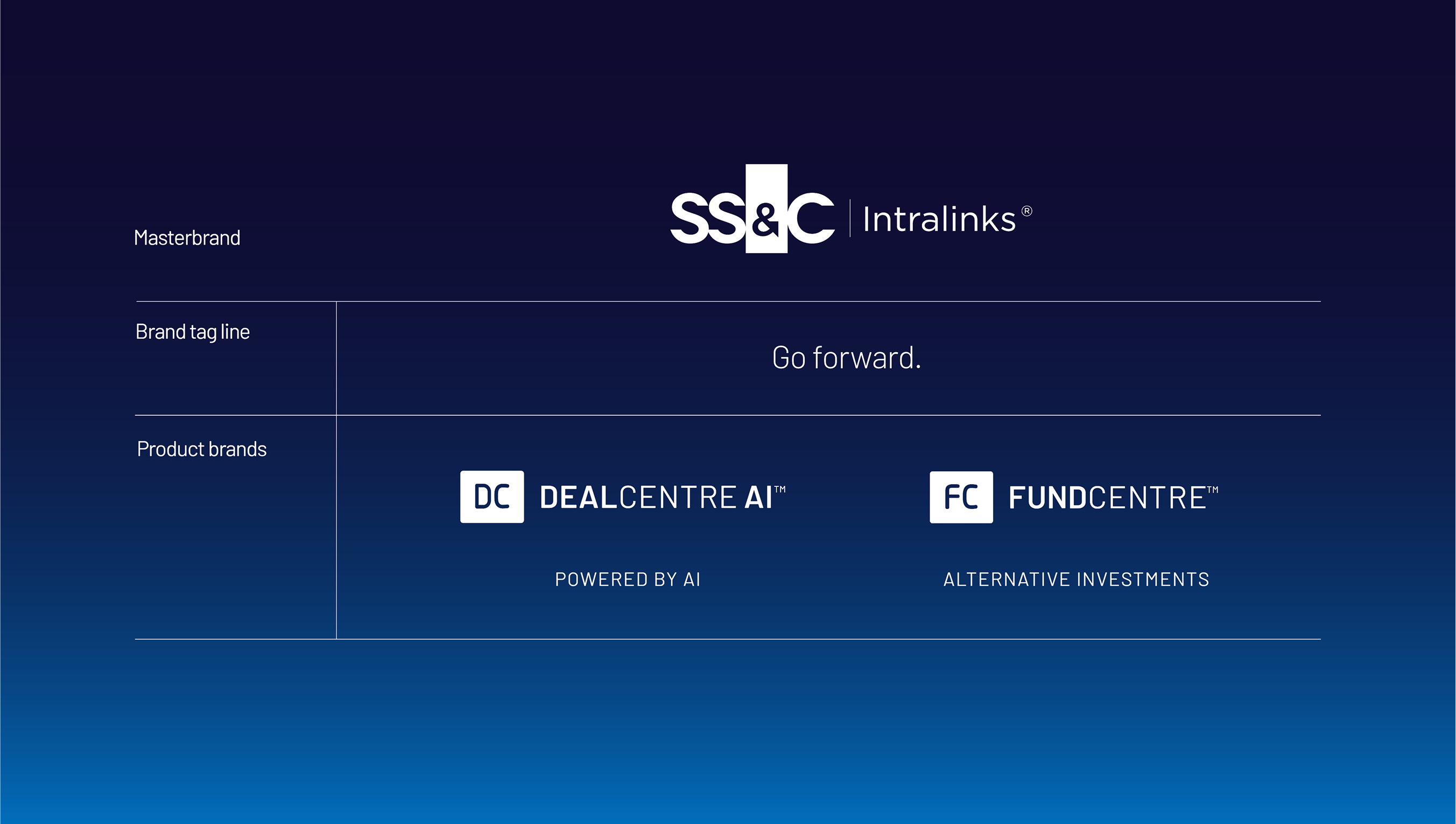

We saw the impact of this with SS&C Intralinks. When we integrated their AI brand into their overall masterbrand, narrative clarity was matched by robust IP documentation and governance alignment.

The integrated positioning gave investors confidence that the business had evolved from a fragmented product suite into a cohesive ecosystem. That confidence supported a significant uplift in valuation over the following year.

By the end of this phase, nothing material should rely on memory or assumption. It should be documented, defensible and ready for scrutiny.

Months 4-0: execute with consistency

In the final four months, the heavy lifting should already be done.

Your structure is defined. Your numbers are disciplined. Your documentation is complete. Now the focus shifts to marketing and communication. How you present the business at this point should reflect the maturity you’ve built over the previous two years.

If you are heading toward acquisition, be explicit about strategic fit:

- Articulate how your positioning strengthens the buyer’s portfolio.

- Show how your products integrate.

- Clarify where synergies sit.

This will make it easy for a potential buyer to see how value compounds post-deal, not just at signing.

If IPO is the route, sharpen the investor narrative.

- Emphasise defensibility, retention strength and competitive differentiation.

- Demonstrate how brand equity supports predictable cash flows and long-term value creation.

Investors will test your claims against your reporting, so ensure the two align.

You should also prepare for scrutiny. Expect questions around regulatory exposure, customer concentration, competitive pressure and growth sustainability. You’ll need to address them directly, supported by documented evidence of mitigation strategies and governance controls. Confidence at this stage comes from preparation, not optimism.

Ultimately, alignment is what holds valuation in place. Brand, operations, governance and financial performance must reinforce one another. When they do, your story remains consistent under pressure. And that consistency is what supports stronger outcomes when the deal closes or the bell rings.

Brand maturity signals acquirers actually value.

By the time you reach diligence, buyers are no longer asking whether your numbers look good, but rather how durable they are.

In 2025-2026, financial services acquirers apply far more sophisticated criteria than simple revenue multiples or customer counts. They assess brand maturity as a proxy for resilience, integration ease and long-term value creation.

Here’s what they are really looking at.

Customer retention as a signal of strength

Retention is both a commercial metric and a brand metric.

When acquirers see annual retention rates above 80%, they interpret that as evidence of embedded relationships and switching costs. It suggests that customers stay because they trust the platform, rely on its workflows and see ongoing value. That reduces perceived integration risk.

By contrast, retention rates in the 50-60% range raise questions. Buyers assume post-acquisition investment will be required to stabilise churn, rebuild trust or reposition the offer. That expectation often translates into lower multiples.

That gap between high and moderate retention can materially affect valuation. Strong retention signals resilience. And resilience supports premium pricing in negotiations.

Net promoter score and customer advocacy.

Retention tells buyers whether customers stay. Net Promoter Score (NPS) and satisfaction metrics indicate whether they would actively recommend you.

An NPS above 50 signals advocacy rather than passive usage. It suggests customers associate your brand with reliability and performance, not simply utility. That advocacy reduces customer acquisition risk and supports expansion opportunities post-acquisition.

During diligence, these metrics become evidence that your growth is not dependent solely on paid acquisition or discounting. They demonstrate brand health that extends beyond transactional relationships.

Brand-driven acquisition efficiency.

Buyers also examine how you acquire customers.

If your growth depends heavily on paid channels with rising acquisition costs, scalability becomes more expensive. If your brand positioning drives inbound demand through referrals, organic search and awareness, your model appears more efficient.

Acquirers look closely at customer acquisition cost relative to competitors and at the contribution of organic channels to pipeline generation. Where brand reduces acquisition dependency on paid media, it strengthens margin confidence.

In simple terms, if your brand does part of the selling for you, your business scales more sustainably.

Regulatory credibility and governance maturity.

In fintech, regulatory posture is inseparable from brand perception.

Buyers evaluate how you communicate compliance, risk management and governance maturity. A proactive compliance stance, transparent reporting and structured oversight signal lower integration risk. They show that the business is used to operating under scrutiny.

Conversely, reactive or poorly documented compliance frameworks create uncertainty. Uncertainty introduces friction. And friction affects valuation.

When brand positioning reflects operational maturity rather than marketing gloss, acquirers see a business that can integrate smoothly into regulated environments.

For example, when Prima, a fast-growing European insurtech, approached us during a period of rapid expansion, their corporate brand needed to match their ambition while speaking credibly to partners, regulators and talent simultaneously.

{kind=link}

{kind=link}

{kind=link}

We developed a clear, candid corporate voice and built a polished, approachable flagship presence that unified audiences. That strengthened positioning demonstrated market maturity at scale. And in environments where trust and regulatory credibility underpin value, that maturity supports valuation confidence.

Fintech brands built for now. Future-ready.

Exit readiness is the disciplined alignment of narrative, numbers and behaviour over time.

The fintechs that achieve stronger outcomes are rarely the loudest. They are the most coherent, with a positioning that reflects their operational reality, reporting that supports their claims, governance structures that stand up to scrutiny, and customer metrics that demonstrate resilience.

They are built for now. Operationally sound. Commercially disciplined. Clear in market.

And they are future-ready. Structured to scale. Positioned to integrate. Prepared to withstand investor questioning without contradiction.

When brand becomes the organising system that connects perception, performance and proof, valuation confidence increases. Not because the story sounds better. But because it holds up under pressure.

That is what sophisticated buyers and public market investors respond to. Alignment. Maturity. Evidence.

And that does not happen in the final four months. It is built deliberately over the 24 before it.

Let’s get things Done & Dusted.

If you are 12-24 months from exit, the time to strengthen your position is now.

We work with fintech scale-ups at pivotal moments of growth and transition. Clarifying strategy. Tightening narrative. Aligning brand, governance and performance so that when scrutiny comes, your story holds.

If you’re preparing for acquisition.If you’re building toward IPO.Or if you want to ensure your valuation reflects the business you’ve built.

Contact us today and let’s assess what your brand needs to take its next step.

Ready when you are.